All hybrid and pure electric cars are more expensive to ensure call your agent back and ask them to quote you on a eco-boost and compare what the rates are then…Sorry, forgot to mention that these numbers are based on monthly payments.

Sponsored

All hybrid and pure electric cars are more expensive to ensure call your agent back and ask them to quote you on a eco-boost and compare what the rates are then…Sorry, forgot to mention that these numbers are based on monthly payments.

Ok. I bailed on F! Call the $0.54/sh a dividend. I may buy some back before close tomorrow (Friday) or in after market session.Last time I bought F at about $9.50 it dropped down to nearly $4, then they suspended paying the dividend,,,,, I just could not convince myself to buy again yesterday.

HRG

massive increase. did you get alternative quotes yet?

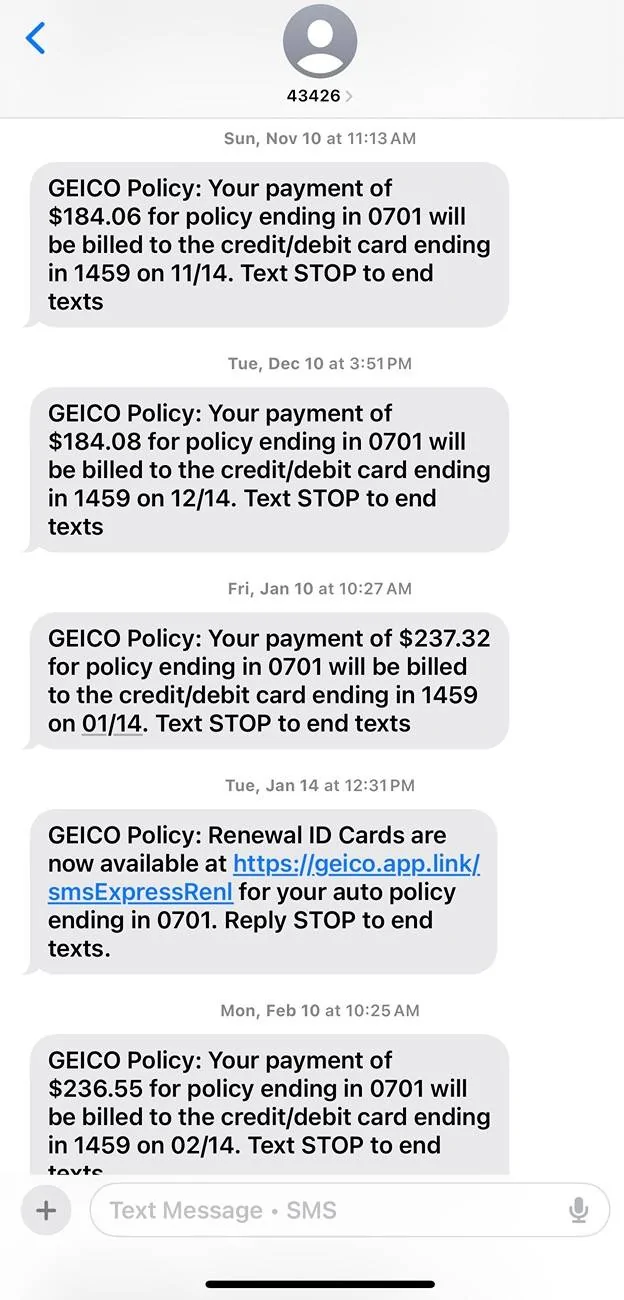

2024 awd ecoboost, 250/500k liability, 1000 comprehensive deductible, 1000 collision, 5k miles per year, divorced male, 39 years driving experience, 1 speeding ticket 2 years ago. 1 not-at fault accident that was paid for by my uninsured motorist policy for about $10k in damages. No dependents. Policy was $184 in 2024, but raised to $236 in 2025 with no changes on driving record. 28.5% annual inflation.

No. It’s on my to do list, but I’ve been procrastinating because the speeding ticket is going to hit 3 years this summer and fall off of my record. Do I get a new company that is cheaper now, then get a second new company after this summer when I can get lower even lower quotes?massive increase. did you get alternative quotes yet?

other than the inconvenience of it, there's no drawback to switching every 6 months if so inclined.No. It’s on my to do list, but I’ve been procrastinating because the speeding ticket is going to hit 3 years this summer and fall off of my record. Do I get a new company that is cheaper now, then get a second new company after this summer when I can get lower even lower quotes?

This.Seems that location makes a huge difference. Living in Houston does definitely not help with low insurance.

because you are likely a long time policy holder and they figure that you're not going to be moving to another company, they love complacency. I'd have called my agent and registered my complaint and ask them what the heck is going on. If I didn't get a satisfactory answer and if they weren't going to lower the rates then I'd go shop around at another company. I have never in 50 years caused an accident, the last ticket I had was 30 years ago, my SF insurance rates are reasonable but I guarantee that if I picked up a ticket or filed a low cost claim (that I wasn't responsible for) and they jacked the ins up substantially I would be on the phone the next day. Hate it when they never 'look back' (50 years!) to offer a discount but are sure to potentially jack up rates if you make one mistake last year.I am 66. 1 speeding ticket in my life for doing 57 in a 55 when I lived in Ohio. 1 ticket for a u-turn on a side street of Richmond VA where I was 1 of 3 pulled over for making a u-turn because the NO UTURN sign was behind a bush. I accident claim when I was rear ended and my insurance did not have to pay 1 penny. 1 hail damage claim. So in 66 years not much. Credit score? 811. So why would State Farm quote me over 1800 a year on a 2024 Maverick in Virginia?

you need to jack up that bodily injury limit - 25K won't fix anything on anyone.Progressive Insurance 500 deductible 500 collision on my 24 XLT @ $175.16/mo. Bodily injury & Property Damage 25K each person 50K each accident

Uninsured motorist 25K each person 50K each accident

using credit scores when they have a long history of your driving history is ridiculous. If you've been with an ins co for 25 years and no or 1 ticket then that's the indication of predicting what kind of a driver you are - not some credit score. There should be a law - you can use the credit score as long as the ins co does not have more that 4 year history on you - else they use your past history. I'm pretty sure if you did have a couple claims and a few tickets in your past buy you had a 850 credit score that they wouldn't be using your credit score to base your rates they'd be using your past history. So - it's one of the other.This.

Your zip code is the single largest factor. It includes the effects from the number of uninsured drivers in your area, and the number of thieves, as well as local driving.

My uninsured motorist coverage (for if one hurts people n my car) is more than my own liability if you look at the breakdown.

The next largest factor is credit score. It sounds odd, but is highly correlated. Several years ago, Teas was going to ban its use tin setting rates. In an odd (for a government) moment of thoughtfulness, the legislature put it off and ordered a study, to be reviewed at the next session.

The study found that credit score was a better predictor of future losses than driving record!

(and when you think of it, someone with a high credit score is more likely to take care of minor things themselves instead of filing a claim than someone with a lower score (again, a broad generalization about groups, not individuals!).

Your driving record then comes in. my policies send a statement of how the increases for various things are calculated.

Age (more as a proxy for driving experience) is also a huge factor until the mid 20s.

As for myself, in a bad neighborhood in Las Vegas, the maverick with two adult drivers with long experience and clean records is close to $200/month--and I have a particularly good independent agent. (Only Amica and California Casualty have ever offered me lower rates).

So the maverick costs significantly more than my six classic cars, valued from $5k to $17k, iirc, with liability on three and just comp on the rest!

Large cities and suburban areas tend to be a couple of times, or more, as expensive as smaller areas. I recall going from $100/month to $30/month, same car, when I left Las Vegas for Ames, IA and graduate school 30 years ago.

in my state your normal health insurance kicks in after PIP, so I carry the minimum allowed for PIP (10k). if anyone is uninsured and riding in my car, they'll obviously still get emergency services and said emergency services would blow through 25k also.you need to jack up that bodily injury limit - 25K won't fix anything on anyone.

Check your rates before going to purchase a new vehicle is a good idea!I actually got quotes from ALL of the 'we will save you hundreds" crowd, State Farm, AAA, Farm Bureau. ALL were more a year than Eire. Progressive? Sure they can save me money by offering the state minimum liability. When i said i have 500k/1 mil coverage their quote was 600 more a year than Eire. I did CALL my agent, not my first rodeo since I bought my first brand new vehicle in 1978 at age 19. I talked to another company's agent and he told me a good story. He has a customer that has 5 autos, 1 boat, 1 motorcycle, him, his wife, 1 college student and 2 high school students on the policy. He traded in for a new Audi so made a change which negates his locked in rate. His insurance went from 4800/year to 11k/year.

in my state your normal health insurance kicks in after PIP, so I carry the minimum allowed for PIP (10k). if anyone is uninsured and riding in my car, they'll obviously still get emergency services and said emergency services would blow through 25k also.

[/QUOT

The difference is the amount you will be owe after the 25k runs out if you are cause of the accident.