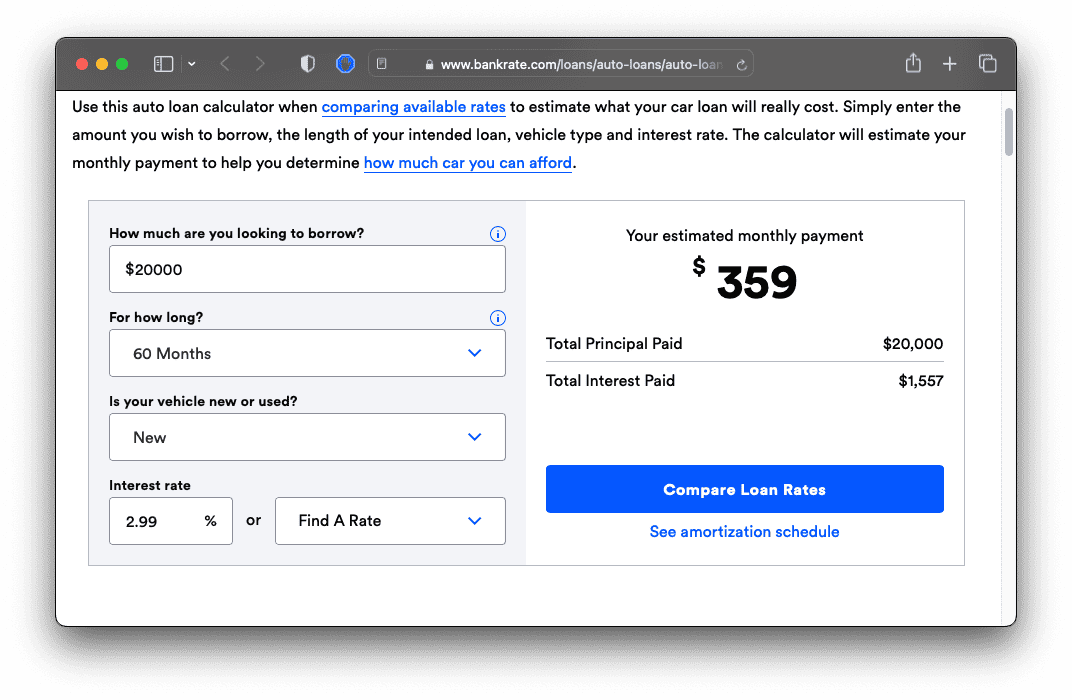

Suggest you check tower credit union I just got pre-approved for 20k with 2.99% for 60 months.

Sponsored

You dont have to card hop to get above 750. You need to occasionally carry a balance, dont miss payments, have enough credit so what you do use is not over 10% of your total, and have a long history with plenty of accounts. I have a 780 coming out of college, I just had 3 cards for rewards. My wife and I both have 820+ scores depending on which score they look at it might be higher. We could both be really methodical about it and try to get higher scores but neither of us care all that much. We just have a few cards each that we use to maximize points and we don't carry balances almost ever, never missed a payment.Not sure how people get scores above 750, honestly. But I also don't card hop like some people do.

Excellent rates. I believe you wont get that from your friendly local finance manager

Maybe for 2023 they are good, but up until 2022, my local credit union consistently had 1.7% apr on refinancing for many yearsExcellent rates. I believe you wont get that from your friendly local finance manager

I haven't missed a payment in over a decade and my balances are next to zero (orthodontist hit me earlier this month). I even have over a decade of solid mortgage payments. In fact, I could literally buy the truck with my available credit card limits if I was stupid enough.You dont have to card hop to get above 750. You need to occasionally carry a balance, dont miss payments, have enough credit so what you do use is not over 10% of your total, and have a long history with plenty of accounts. I have a 780 coming out of college, I just had 3 cards for rewards. My wife and I both have 820+ scores depending on which score they look at it might be higher. We could both be really methodical about it and try to get higher scores but neither of us care all that much. We just have a few cards each that we use to maximize points and we don't carry balances almost ever, never missed a payment.

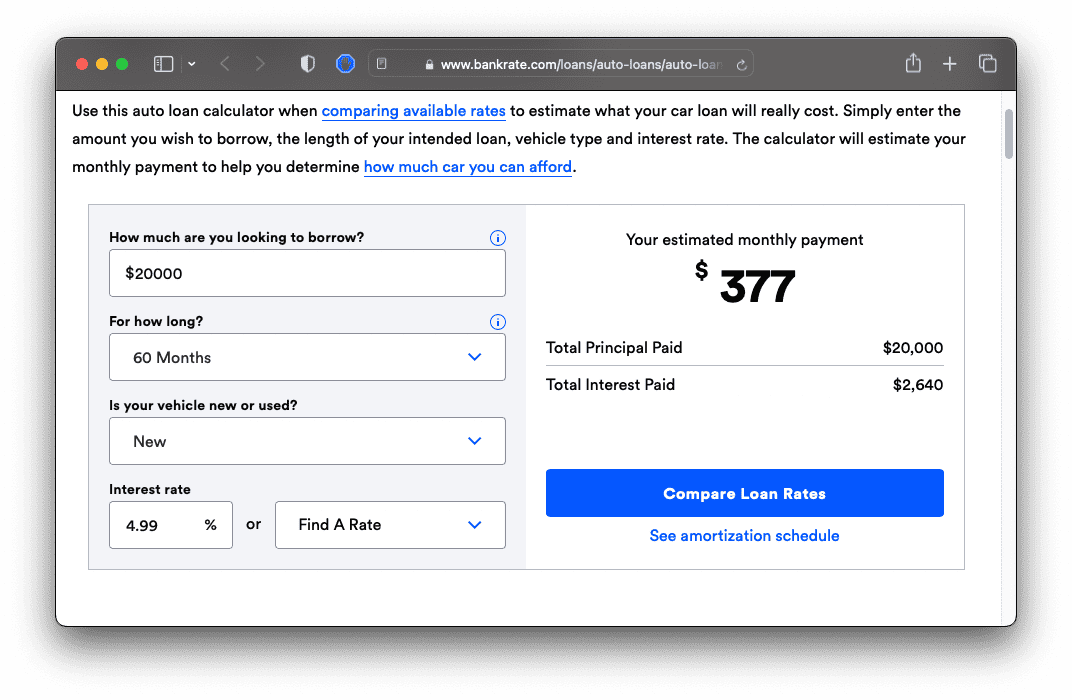

Wow, that's a lot in interest payments.i got 4.99% for 84 months with ford credit.

Yeah the fed rate being basically zero for a while will do that. Rates will only continue to go up in 2023. Fed expected to raise rates 25bps twice this year.Maybe for 2023 they are good, but up until 2022, my local credit union consistently had 1.7% apr on refinancing for many years

Don't need to card hop just get juicy sign up bonuses and don't close the account. Get cards with no annual fee so after you use it get the bonus leave it open. That will build your history as well as increase your overall credit limit. If you spend $2000 and all the limits of your card together are $10k credit limit you look like you use 20% of your credit. However if you spend the same $2k and have $100k limit you just look like you spend 2% of your limit a month. Big difference in the eyes of the banks. Takes a little time but the rewards are huge. It's a fun game to max out rewards for categories like gas spending or grocery. There are cards out there for every purpose. I suggest watching some of the credit card videos on YouTube to get started. Right now the highest ever offer for IHG hotels card just launched . 175k bonus for spending $3k in 3 months annual fee is $99 comes with a bunch of perks main one is status and a free night every year. They also have a free version which will earn 120k after $2k spend in 3 months. Those are easy targets with how expensive just living is now. Those points would come in handy on a road trip with the MaverickNot sure how people get scores above 750, honestly. But I also don't card hop like some people do.

. Just make sure the hotel chain has properties where you would like to go and that you can hit that spend without spending extra. If you are interested in that deal just Google 175k chase and IHG it will pop up. I usually like to wait until it gets close to insurance payments time to apply for a card. Or most dealers will allow $3k-$5k on a card for down payment bam! Spending done in one transaction. Everybody should be doing that when they go pickup their mavericks. Huge sign up bonuses earned and a new truck to drive home! I'd wait until the truck is in transit so you can get the timing right. Have fun!

. Just make sure the hotel chain has properties where you would like to go and that you can hit that spend without spending extra. If you are interested in that deal just Google 175k chase and IHG it will pop up. I usually like to wait until it gets close to insurance payments time to apply for a card. Or most dealers will allow $3k-$5k on a card for down payment bam! Spending done in one transaction. Everybody should be doing that when they go pickup their mavericks. Huge sign up bonuses earned and a new truck to drive home! I'd wait until the truck is in transit so you can get the timing right. Have fun!Do you live in Maryland? Can anyone join? Looks like DOD and military mostly.Suggest you check tower credit union I just got pre-approved for 20k with 2.99% for 60 months.

I believe the USAA rate has a 1300 loan initiation fee which makes it more like a 7% rate.USAA bank had 4.74% for up to 63 months last week and a lock on it for 45 days. Dealer was saying 5.7 was the best they were seeing at that time. Locked in the 4.74 .

I do not have an origination fee on the locked in 4.74% rate. Generally USAA and Penfed are close in their rates. This time USAA was the better deal.I believe the USAA rate has a 1300 loan initiation fee which makes it more like a 7% rate.

Worst case is a $35 donation that is recouped many times over in interest if you can still get 2.99% for 60 months.Do you live in Maryland? Can anyone join? Looks like DOD and military mostly.

https://www.towerfcu.org/eligibility/Eligibility

- Employees of member companies

- Members of organizations in our field of membership

- Immediate family members of existing members (spouse, child, sibling, parent, grandparent, grandchild, stepchild, stepparent, stepsibling and adopted child)

- Individuals living in household of an existing member

- Not eligible via above options? Become a member of TowerCares Foundationwith a $35 donation. Make your donation and return here to Become a Member.

https://www.towerfcu.org/borrow/loan-rates/#1481818323110-6112493a-d3be�

New Cars and Trucks Term

(in months)APR%

(as low as)Monthly Payment

(per $1,000 borrowed)36 2.24 $28.75 48 2.99 $22.13 60 2.99 $17.96 72 3.49 $15.41 84 4.99 $14.13

Yes they have an option to donate 35$ for tower foundations as the last resort to be a member.Do you live in Maryland? Can anyone join? Looks like DOD and military mostly.

2.99% to 4.99% is over $1,000 for $20,000 borrowed over 60 months. $1,083 to be precise. Interestingly, $1,085 (+$2) was the up-charge for EcoBoost when 2022 Maverick launched. The difference in interest increases linearly with increases in the amount borrowed. $30,000 would be 50% more interest, for instance.No doubt. 2.99 is an incredible rate at this point in time. But also, folks need to keep in mind that the difference between 2.99 and 4.99 in total paid will be less than a thousand bucks, and that is IF you actually carry the loan to full term.

Do you interact with people in real life like this? My apologies for my quick and imprecise head math. The point of my comment was pretty simple- keep in mind that the ultimate difference between a couple percentage points on a loan is often less than one might guess. Not saying getting a better loan rate is a bad idea, just that it is about 50 cents per day. If that is a lot to you, fine, if not, also fine.