Not sure what you mean here. The link says nothing about dealers being required to accept the Ford Pass card for down payments.

Sponsored

Last edited:

Not sure what you mean here. The link says nothing about dealers being required to accept the Ford Pass card for down payments.

and after the cc and new purchase points posted I applied them to my warranty. After this posts and RealTruck gets the new rails for the x4s I'll get a bed cover. That & maybe some misc will get me the $200 statement credit... all in about a $600 savings by using the card an paying it off with each statement.Not sure what you mean here. The link says nothing about dealers being required to accept the Ford Pass card for down payments.

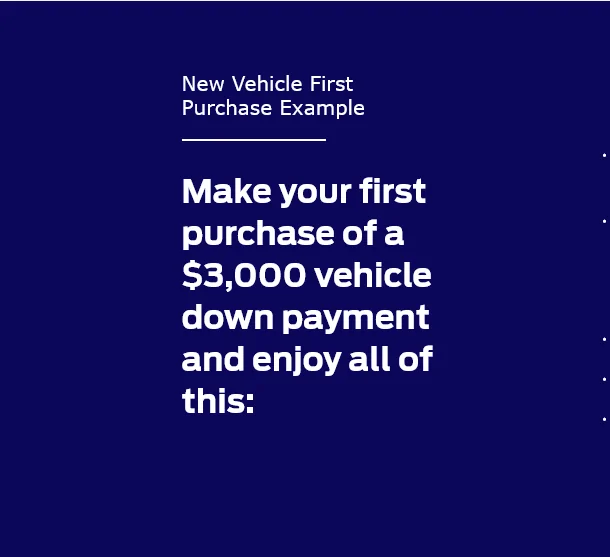

Yeah, all due respect: this means nothing. It literally says “Example” at the top. They’re literally giving you a theoretical of how you could earn points, not setting out limits dealers must live to. And there wouldn’t and shouldn’t be any “blaming Ford”; individual dealers decide issues like this. Has nothing to do with Ford. And they could very well decide they’ll allow you to do $3k, or $5k, or hell, the whole thing, but then charge you the 2.9% they pay.by posting this they state you can, not that you dealer is required but they lose any argument of blaming Ford. My dealer caved as soon as I showed it to him.

The use of credit cards is a Dealer Option. Most likely influenced by the franchise agreement and the limits placed upon manufacturer by the laws which restrict them from telling dealers what they "want them to do" such as "sell only at MSRP".Wow, reading these posts, it clearly varies from place to place.

At my Ford dealer, I put $12k down, spread over two credit cards. I had the cash in the bank to write a check, but using the credit card(s) was actually their suggestion "if I wanted the points or cashback." They would've let me buy the whole truck on credit cards, with a $10k max per card.

They charged zero convenience fee, which is about the only good thing I can say about them.

I'm not sure, but if you put 5K on the card, that means you have 2 payments to make each month. 1 for the cridit card, and 1 for the auto loan. (the loan will be 5K less) $22K. I'm sure the auto finance will give you a better rate in the long run.I plan to use the Ford Pass Rewards card to pay part of the purchase price of my truck that will be arriving soon so I can get the rewards. I pinged my dealer to ask what the max is I could put on the card, as I know some dealers charge a fee over XXXX dollars. Their reply has me a bit curious: they say if I am financing at all, whether my own financing, Ford Credit, or a bank my dealer works with and arranges, the max is $500. If I am paying cash, the max is $5000. That seems odd to me; I would almost think it should go the other way: if I finance using a bank they arranged, they get a kickback, so I'd think would be more willing to eat the credit card fees of a larger credit card payment. Am I missing something? Not planning on causing a stink as they have been GREAT to deal with (MSRP, no add-ons, $27 doc fee). Just curious what the angle is I'm missing.

I have the cash for it, just want the rewards to get some accessories.I'm not sure, but if you put 5K on the card, that means you have 2 payments to make each month. 1 for the cridit card, and 1 for the auto loan. (the loan will be 5K less) $22K. I'm sure the auto finance will give you a better rate in the long run.

At the dealer I was at, the lenders ("lenders" plural, since dealers can and will look for multiple options) would've had no way of knowing how I was paying my down payment. All they would've seen was a credit report and a financed amount vs. the value of the vehicle they are putting the lien on. It wasn't until I got to the F&I office that I was even asked how I was paying. By that point, the lender and terms were all decided.IF you look at it from the financing bank's point of view. I would guess that they look at putting the down payment on a credit card as if that person could not afford the down payment. If I was making someone a loan I would not want that person to use a credit card for the down payment because I would not be sure if they could actually afford it regardless if they pay it off right away. If the person cant really come up with the down payment and put it on a credit card that would put them in a bad place where they would have to payback a small loan with extra high credit card interest rates and the car payment.

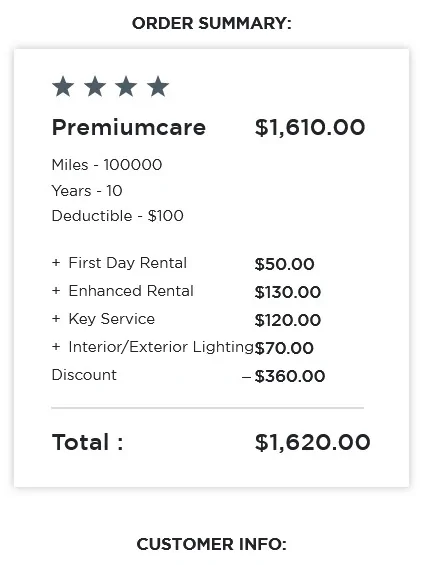

The dealer could care less what credit card you use. Ford card is Omaha bank Visa not Ford. Most dealers will charge a fee which is (3% at my dealer) for any purchase deposit etc.If you use the Ford credit card you can charge up to $3000 towards the down payment, if your dealer has a problem with it go to Ford credit card site, scroll down and show it to them. Don't buy the warranty, when you pay off the cc you will receive bonus points in your app... then go to Granger and get your warranty and apply the points.

by posting this they state you can, not that you dealer is required but they lose any argument of blaming Ford. My dealer caved as soon as I showed it to him.

You probably paid a fee. Credit card companies don't loan $ for free. Any dealer that doesn't charge a fee ought to find a new GM.

You probably paid a fee. Credit card companies don't loan $ for free. Any dealer that doesn't charge a fee ought to find a new GM.