- First Name

- R

- Joined

- Sep 1, 2023

- Threads

- 20

- Messages

- 1,075

- Reaction score

- 1,463

- Location

- California

- Vehicle(s)

- 2024 Maverick XL 2.0 AWD 4K CP360

- Engine

- 2.0L EcoBoost

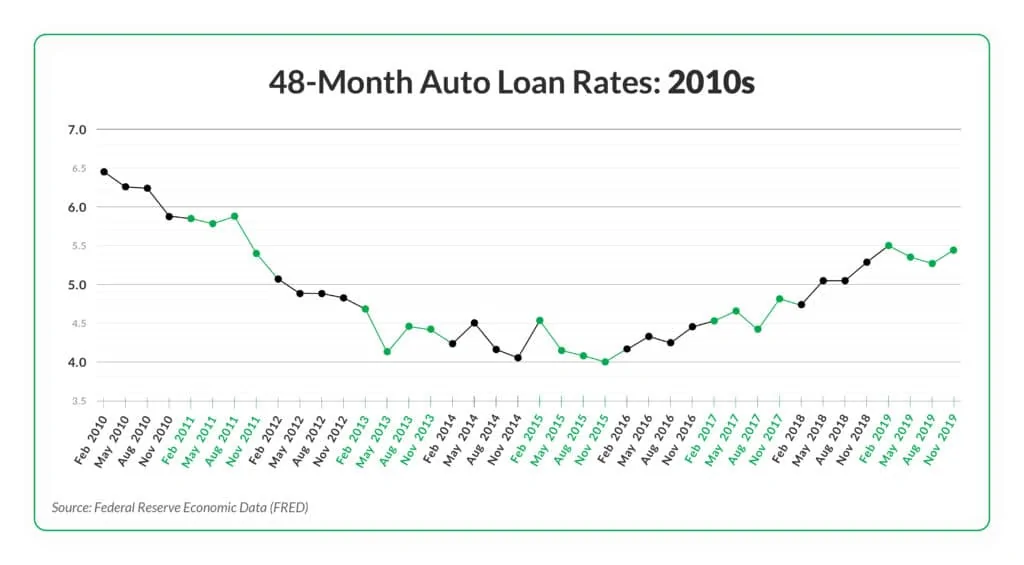

I think the biggest struggle that people have with the high interest rate is that the interest is for something that costs a lot more. For easy math, 10% of 100,000 (10,000) is still less than 5% of 500,000 (25,000). In terms of a 30 year house loan, the majority of the monthly payment is interest at first, and when that interest triples, your house payment does as well.

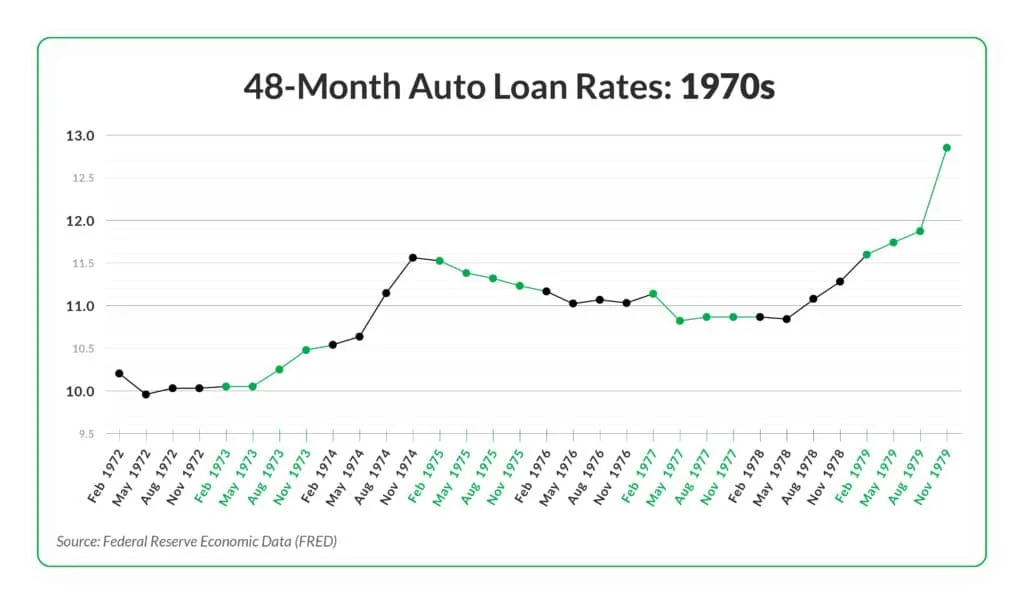

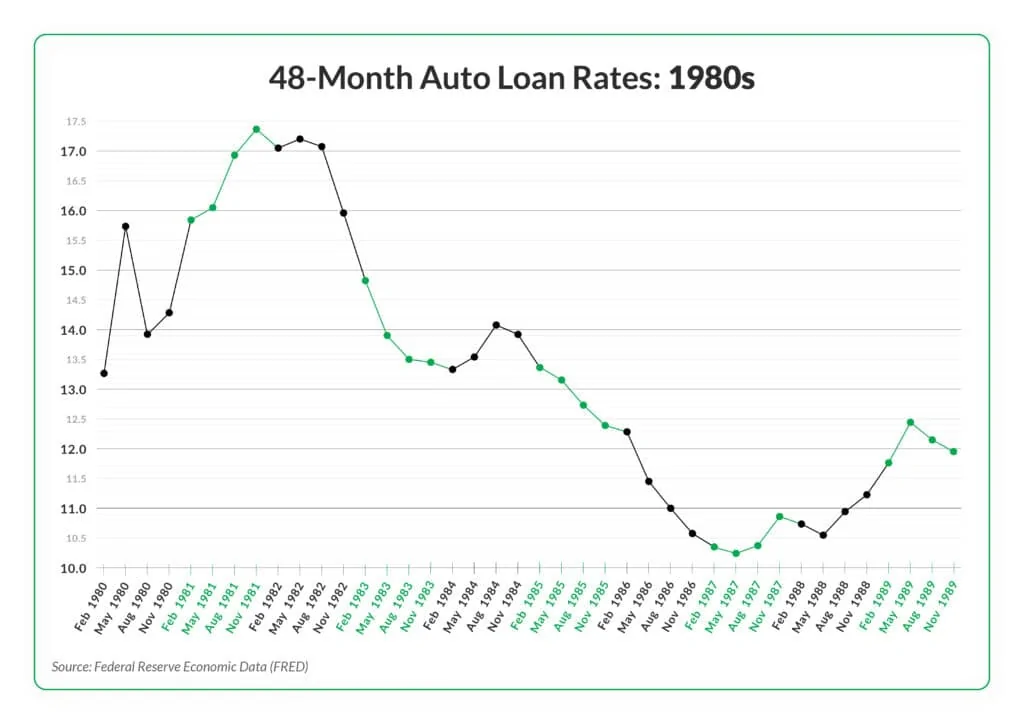

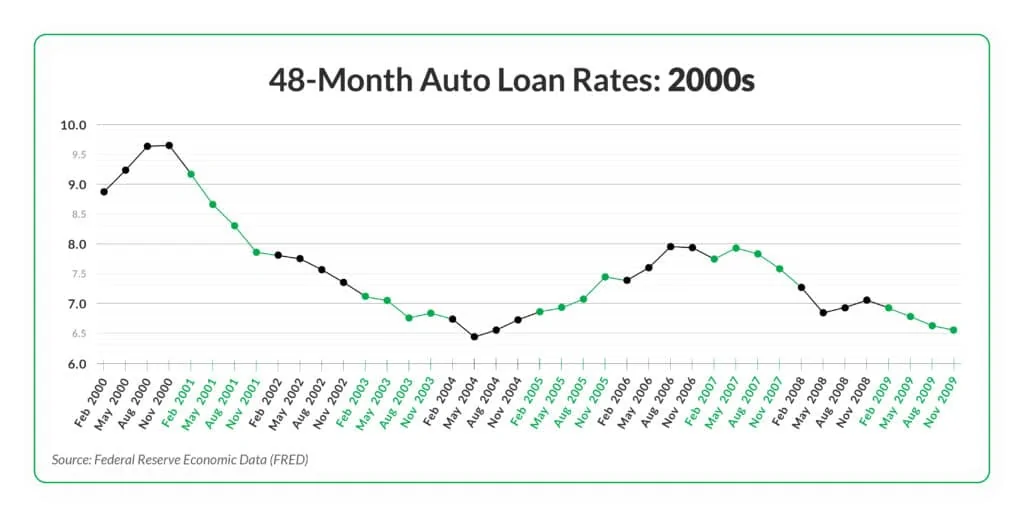

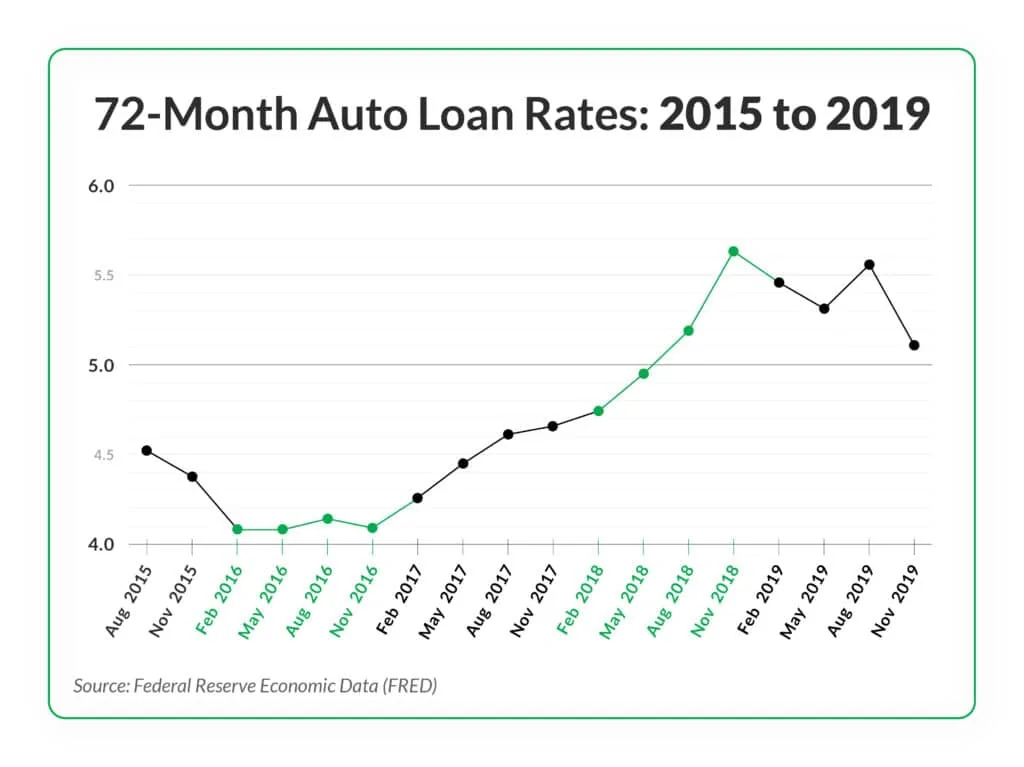

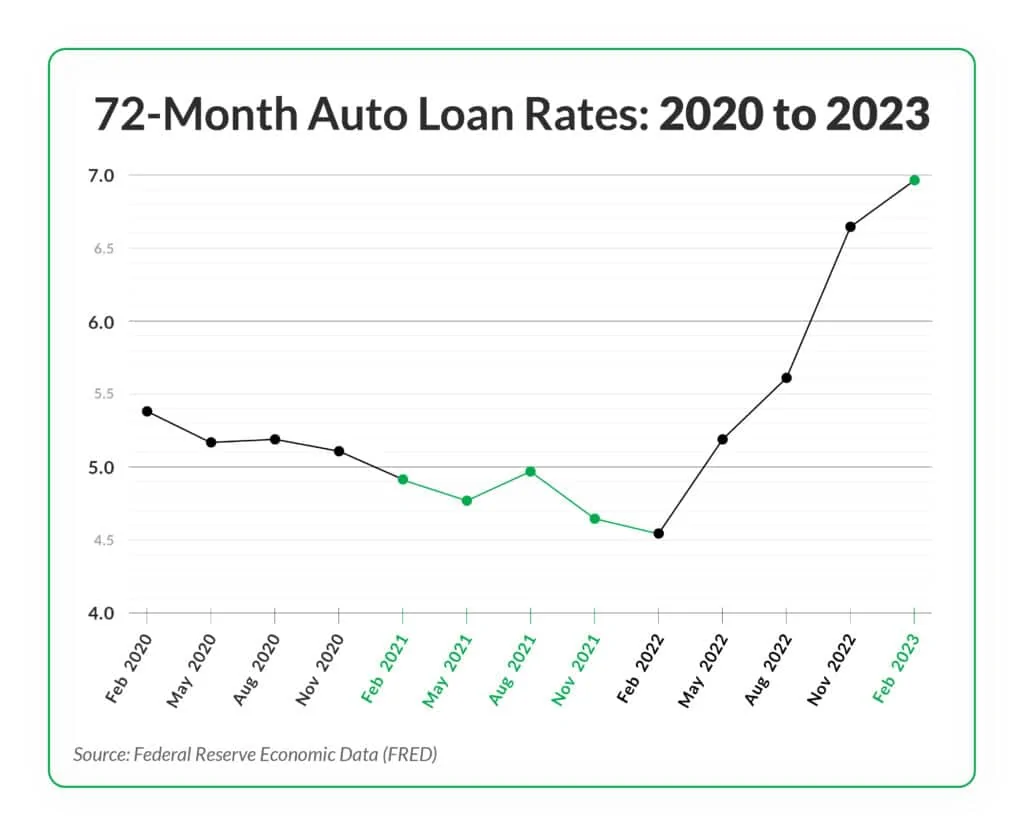

The banks are making a lot more with these high interest rates today, than they were back in the 80s. There is a reason that people are extending their loans, and it isn’t because cars last longer.

congratulations @SLINGSHOT for paying off your house and being able to pay cash for everything since then (100% sincere). My 5 year plan is to be able to do the same thing as you.

The banks are making a lot more with these high interest rates today, than they were back in the 80s. There is a reason that people are extending their loans, and it isn’t because cars last longer.

congratulations @SLINGSHOT for paying off your house and being able to pay cash for everything since then (100% sincere). My 5 year plan is to be able to do the same thing as you.

Sponsored

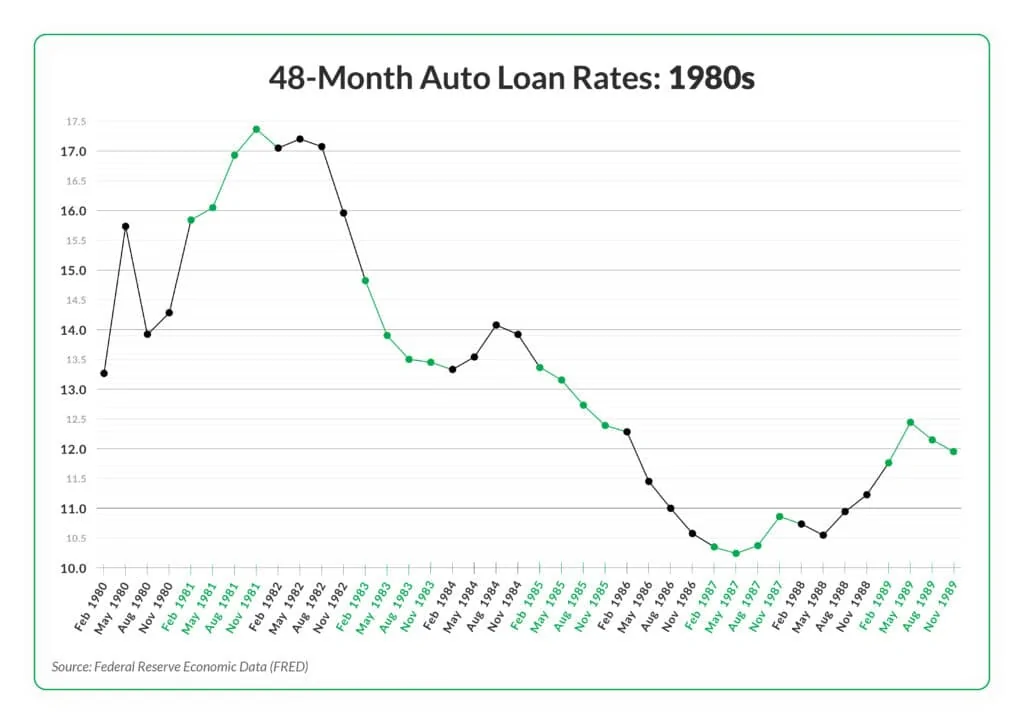

That was the rate my parents mortgage was in 1980 when they bought their first home. People crying over 5-8% just makes them laugh.

That was the rate my parents mortgage was in 1980 when they bought their first home. People crying over 5-8% just makes them laugh.