- Thread starter

- #1

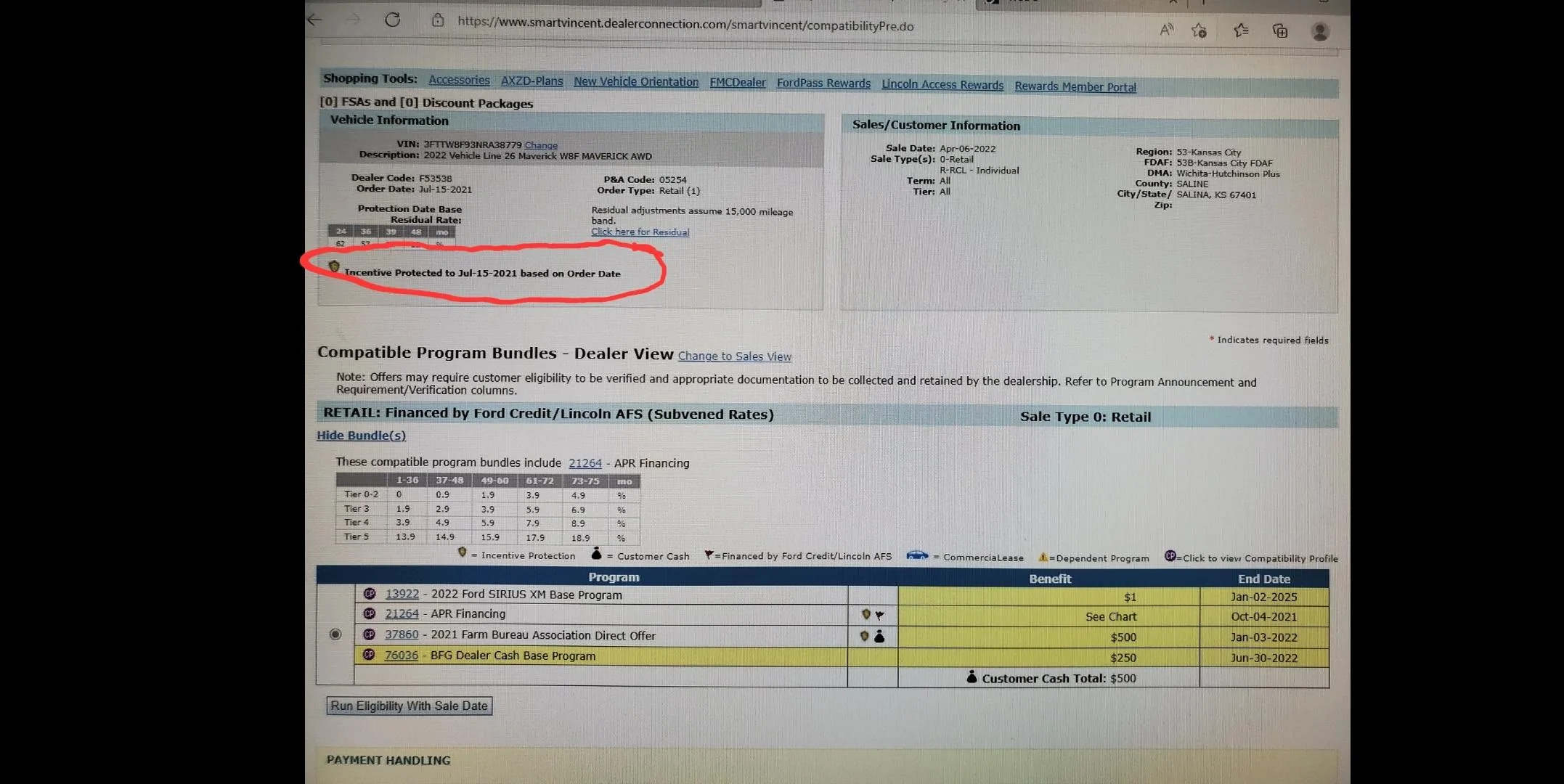

Here's a question I am sort of hoping @fordvideoguy will answer, but I'm posting here with the thought that the information will be helpful to anyone still waiting for their Maverick order to be built. It's also possible that other dealers active on this forum and/or @Ford Motor Company may have additional information to add.

My question is this: if you receive a private offer (cash rebate) from Ford, or have access to the Farm Bureau $500 certificate, can you use that AND still get protected for Ford Credit financing based on your order date? I have seen several posts recently from people whose dealers have told them it's either one or the other. Use the cash rebate OR get the old financing rates (0% for 36, .9% for 48, 1.9& for 60, etc.).

So, for those of us waiting for our trucks and want to finance at the protected rates, is it worth us even bothering to join the Farm Bureau or try to submit a private offer to our dealer? Or are we giving up the ability to use the old finance rates if we do that?

Thanks in advance for anyone who can shed DEFINITIVE light on this!

My question is this: if you receive a private offer (cash rebate) from Ford, or have access to the Farm Bureau $500 certificate, can you use that AND still get protected for Ford Credit financing based on your order date? I have seen several posts recently from people whose dealers have told them it's either one or the other. Use the cash rebate OR get the old financing rates (0% for 36, .9% for 48, 1.9& for 60, etc.).

So, for those of us waiting for our trucks and want to finance at the protected rates, is it worth us even bothering to join the Farm Bureau or try to submit a private offer to our dealer? Or are we giving up the ability to use the old finance rates if we do that?

Thanks in advance for anyone who can shed DEFINITIVE light on this!

Sponsored