Sponsored

How much is a 2023 Ford XL Base model Maverick?

- Thread starter Jimmy hayes

- Start date

- Watchers 3

- First Name

- Jimmy

- Joined

- Jul 10, 2022

- Threads

- 1

- Messages

- 6

- Reaction score

- 0

- Location

- Largo Florida

- Vehicle(s)

- Ford F150

- Thread starter

- #17

What can the dealership add like fees?

- First Name

- Jimmy

- Joined

- Jul 10, 2022

- Threads

- 1

- Messages

- 6

- Reaction score

- 0

- Location

- Largo Florida

- Vehicle(s)

- Ford F150

- Thread starter

- #18

Plus dealership fees?How much is a 2023 Ford xl base model Maverick

- First Name

- Austin

- Joined

- Jun 19, 2022

- Threads

- 3

- Messages

- 27

- Reaction score

- 15

- Location

- Tallahassee

- Vehicle(s)

- 2003 Toyota 4Runner

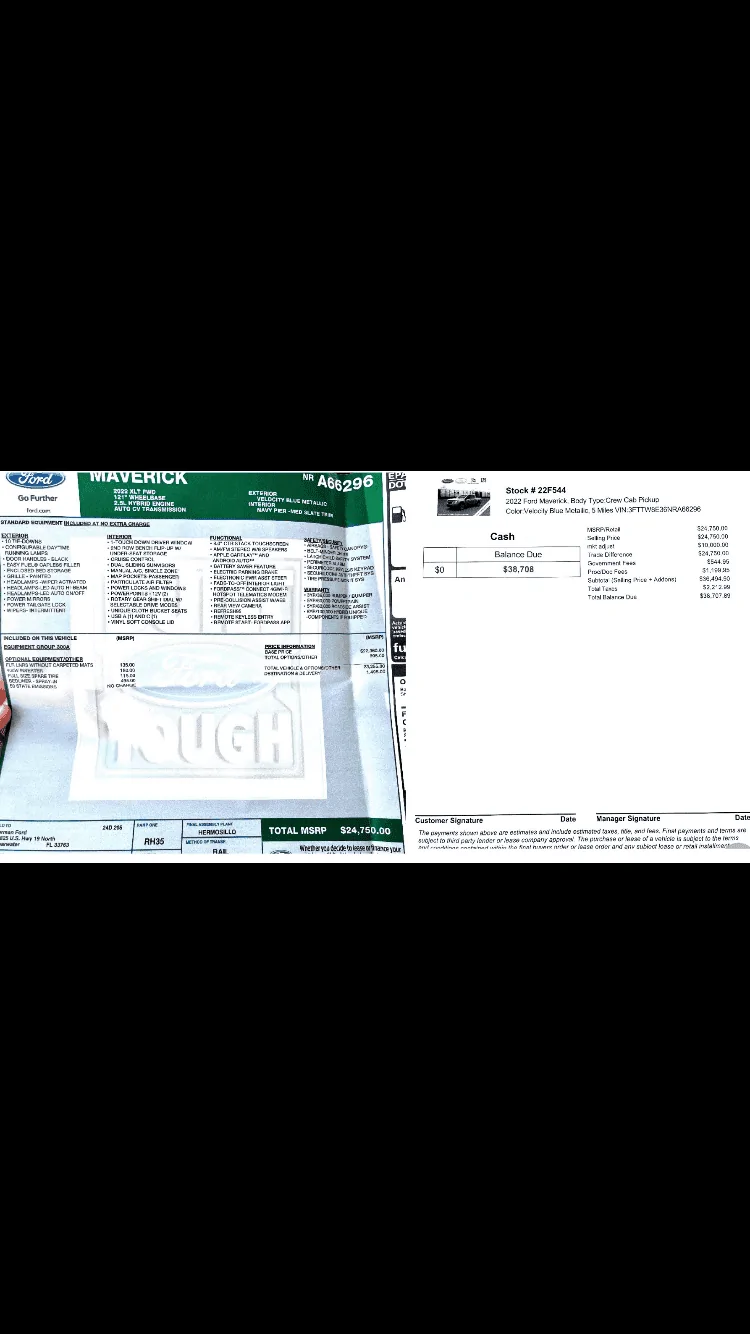

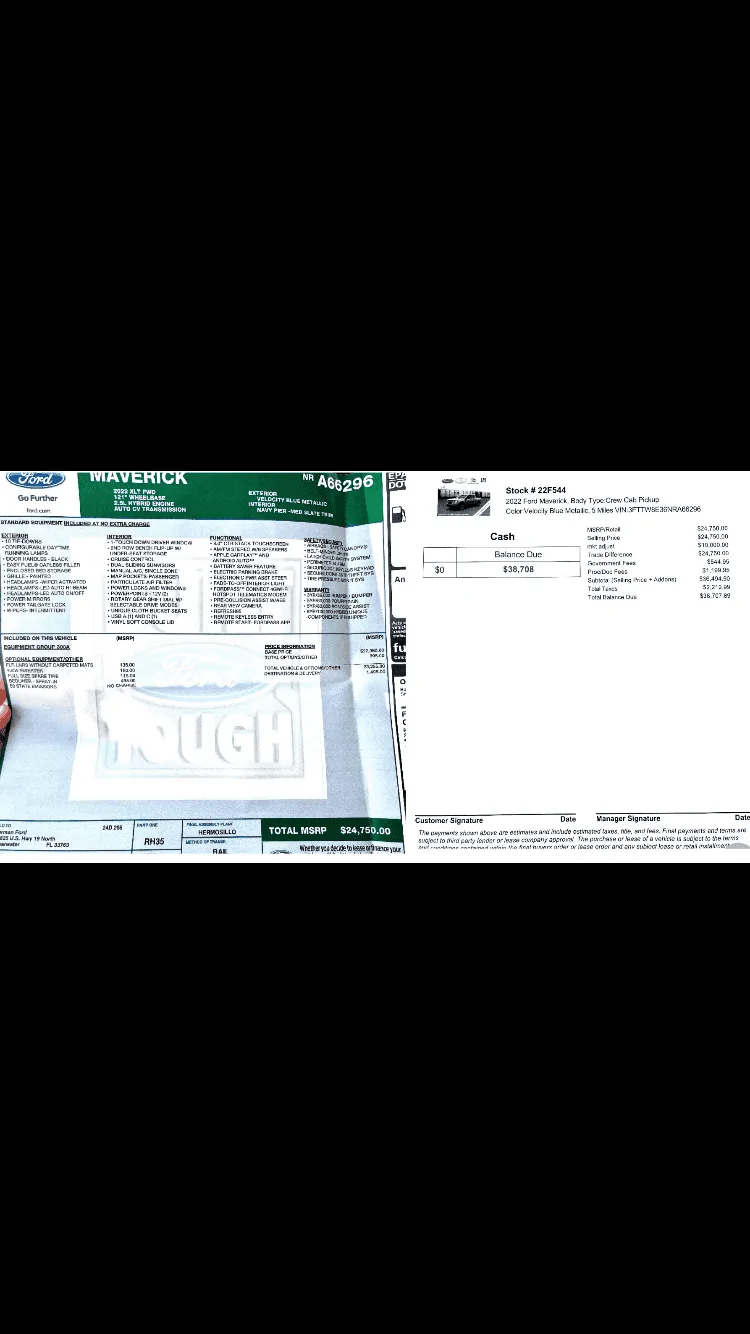

Dealerships can add a ton of fees. I've called probably 30 dealerships between Florida and Georgia asking to be added to a call back lists in case someone declines their Maverick order, and a majority of dealerships I've talked to are adding an additional 5-7K "market adjustment" to the cost of the Maverick. Some dealerships all the way up to 10k extra. One dealership called me and left a voicemail, asking if I was interested in an XLT Hybrid that honestly should have been no more than 25-27k, and they had it listed at 42k.What can the dealership add like fees?

Some will also tell you they won't add a dealership markup like above, but they'll add thousands of dollars worth of equipment to the truck to jack the price up, when the equipment they're adding isn't anywhere near what they say it's worth.

- First Name

- Jimmy

- Joined

- Jul 10, 2022

- Threads

- 1

- Messages

- 6

- Reaction score

- 0

- Location

- Largo Florida

- Vehicle(s)

- Ford F150

- Thread starter

- #20

Yes I ran into a huge 10,000 markup on a 2022 XLT

Sponsored

- First Name

- Jimmy

- Joined

- Jul 10, 2022

- Threads

- 1

- Messages

- 6

- Reaction score

- 0

- Location

- Largo Florida

- Vehicle(s)

- Ford F150

- Thread starter

- #21

- First Name

- Jimmy

- Joined

- Jul 10, 2022

- Threads

- 1

- Messages

- 6

- Reaction score

- 0

- Location

- Largo Florida

- Vehicle(s)

- Ford F150

- Thread starter

- #22

How much is a 2023 Ford xl base model Maverick

- First Name

- Mark

- Joined

- Jun 28, 2021

- Threads

- 15

- Messages

- 3,119

- Reaction score

- 8,416

- Location

- Clearwater FL

- Vehicle(s)

- 2023 Maverick XL Hybrid

- Engine

- 2.5L Hybrid

How much you got?How much is a 2023 Ford xl base model Maverick

- First Name

- Dave

- Joined

- Jul 29, 2021

- Threads

- 6

- Messages

- 207

- Reaction score

- 374

- Location

- Barberton, OH, US

- Vehicle(s)

- '73 Ford Mustang

- Engine

- 2.5L Hybrid

Last time inflation was this high, automakers always split the next year increase into two, with about half on July 1 and the other half on next model year announcement, plus a significant destination charge increase.

All is speculation until August 2, 2022, but my prediction for that date on a 2023 is:

2023 Maverick XL Hybrid: $21,995

Destination charge: $1,695

Total: $23,690

Maybe more.

Last edited:

- First Name

- Dave

- Joined

- Jul 29, 2021

- Threads

- 6

- Messages

- 207

- Reaction score

- 374

- Location

- Barberton, OH, US

- Vehicle(s)

- '73 Ford Mustang

- Engine

- 2.5L Hybrid

Last time inflation was this high, automakers always split the next year increase into two, with about half on July 1 and the other half on next model year announcement, plus a significant destination charge increase.

All is speculation until August 2, 2022, but my prediction for that date on a 2023 is:

2023 Maverick XL Hybrid: $21:995

Destination charge: $1,695

Total: $23,690

Maybe more. Why? Because they can, and I suspect the margins are still tight at that price.

Sponsored

- First Name

- Dave

- Joined

- Jul 29, 2021

- Threads

- 6

- Messages

- 207

- Reaction score

- 374

- Location

- Barberton, OH, US

- Vehicle(s)

- '73 Ford Mustang

- Engine

- 2.5L Hybrid

But, I could be wrong.

The good old days! I was building houses and was paying up to 18-21% interest. On spec homes I could have it built in fewer than 75 days (gotta have good subs and be on your toes and no constrained items or be flexible). Also helped that most building was being shut down and subs were everywhere. I once caught an electrician helping plumber finish so he could start with electrical sooner. After five or six houses with same subs they all new each other's phone numbers and would call each other to schedule their time. I discovered that the interest rate was not a problem it was the number of days you owed the money that mattered. Materials and some of the labor was on monthly accounts and I could close house some times before I had received all the invoices (like free from interest money). I am fearful of the increased expenses that Ford will have to pass through on the 2023's! Hopefully volume will help keep costs down.I believe that is what FVG said on his live show last Tuesday. What we are seeing currently reflects the MY23 increase, at least for a while. Order early and lock that bad boy in.

What I am thinking about now is what FordCredit will be offering for interest terms come August 2. Gotta lock that in as well as I can only imagine what interest rates will be in a year or so when my Maverick comes in. I am old enough to have nightmares of the Carter days and 15% interest rates. Doubt it would come to that, but many of us doubted it would come to that 43 years ago but surprise, surprise. I bought house in '79 at 11% interest. Now that hurt.

True story right there on the length of time you own the money.The good old days! I was building houses and was paying up to 18-21% interest. On spec homes I could have it built in fewer than 75 days (gotta have good subs and be on your toes and no constrained items or be flexible). Also helped that most building was being shut down and subs were everywhere. I once caught an electrician helping plumber finish so he could start with electrical sooner. After five or six houses with same subs they all new each other's phone numbers and would call each other to schedule their time. I discovered that the interest rate was not a problem it was the number of days you owed the money that mattered. Materials and some of the labor was on monthly accounts and I could close house some times before I had received all the invoices (like free from interest money). I am fearful of the increased expenses that Ford will have to pass through on the 2023's! Hopefully volume will help keep costs down.

i'm hoping Hermasillo starts putting some of their growing pains behind them of which I am sure they have had their share and things move along a little more efficiently down the road. I am also sure more than a few Ford Execs have had a few sleepless nights over all this down south of the border. As for supply chain items, vendors coming through with their promised deliveries and the never ending chip shortage here's hoping things start to turn around a bit. Time will tell.

- First Name

- Howard

- Joined

- Oct 4, 2021

- Threads

- 30

- Messages

- 1,236

- Reaction score

- 1,395

- Location

- Brookhaven Lake O' the Pines, Texas

- Website

- www.hchaney.com

- Vehicle(s)

- 2022 Maverick XL, VB, 2.0 EB

- Engine

- 2.0L EcoBoost

Bob, I was one of those electricians that needed to get to the job as soon as possible in those days. You had to be inventive to make money. Survived long enough to sell our design, contracting, service, and lighting store. Thanks for the memories.The good old days! I was building houses and was paying up to 18-21% interest. On spec homes I could have it built in fewer than 75 days (gotta have good subs and be on your toes and no constrained items or be flexible). Also helped that most building was being shut down and subs were everywhere. I once caught an electrician helping plumber finish so he could start with electrical sooner. After five or six houses with same subs they all new each other's phone numbers and would call each other to schedule their time. I discovered that the interest rate was not a problem it was the number of days you owed the money that mattered. Materials and some of the labor was on monthly accounts and I could close house some times before I had received all the invoices (like free from interest money). I am fearful of the increased expenses that Ford will have to pass through on the 2023's! Hopefully volume will help keep costs down.

It was scary times. The day before closing I would go to bank and get enough cash to pay all bills so I could be certain I could pay them. ( There was an affidavit in the closing paper work in which I certified that everything had been paid for so I was ready if banker shut me down. They were getting notices occasionally from fed to cut back loans.). I also had a tape and texture sub who would not bill me and at one point I had 4-5 houses I had closed and he called and asked for money on one of them. When I paid him in cash I asked him why he wouldn't bill me and he replied "xyz builder cannot pay and I need the money. Since you always pay when I ask you are my emergency banker".Bob, I was one of those electricians that needed to get to the job as soon as possible in those days. You had to be inventive to make money. Survived long enough to sell our design, contracting, service, and lighting store. Thanks for the memories.

Sponsored

Similar threads

- Replies

- 40

- Views

- 10,801

- Replies

- 6

- Views

- 6,134